Focus: Time Series#

ARIMA#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

import statsmodels.tsa.api as smts

import statsmodels.tsa.stattools as smtst

from statsmodels.tsa.statespace.sarimax import SARIMAX

from statsmodels.stats.diagnostic import acorr_ljungbox

from itertools import product

import tqdm

df = pd.read_csv('time_series.csv', index_col='Date', parse_dates=True)

df

| y | |

|---|---|

| Date | |

| 2012-10-02 | 1938.0 |

| 2012-10-03 | 3521.0 |

| 2012-10-04 | 3475.0 |

| 2012-10-05 | 3148.0 |

| 2012-10-06 | 2006.0 |

| ... | ... |

| 2014-05-27 | 5032.0 |

| 2014-05-28 | 4008.0 |

| 2014-05-29 | 4587.0 |

| 2014-05-30 | 4869.0 |

| 2014-05-31 | 2887.0 |

607 rows × 1 columns

def tsplot(y, lags=None, figsize=(20, 10), title=None):

fig = plt.figure(figsize=figsize)

layout = (2, 2)

ts_ax = plt.subplot2grid(layout, (0, 0), colspan=2)

acf_ax = plt.subplot2grid(layout, (1, 0))

pacf_ax = plt.subplot2grid(layout, (1, 1))

y.plot(ax=ts_ax)

p_value = smts.adfuller(y)[1]

if title is None:

title = 'Time Series Analysis Plots'

ts_ax.set_title('{0}\n Dickey-Fuller: p={1:.5f}'.format(title, p_value))

smts.graphics.plot_acf(y, lags=lags, ax=acf_ax)

smts.graphics.plot_pacf(y, lags=lags, ax=pacf_ax)

plt.tight_layout()

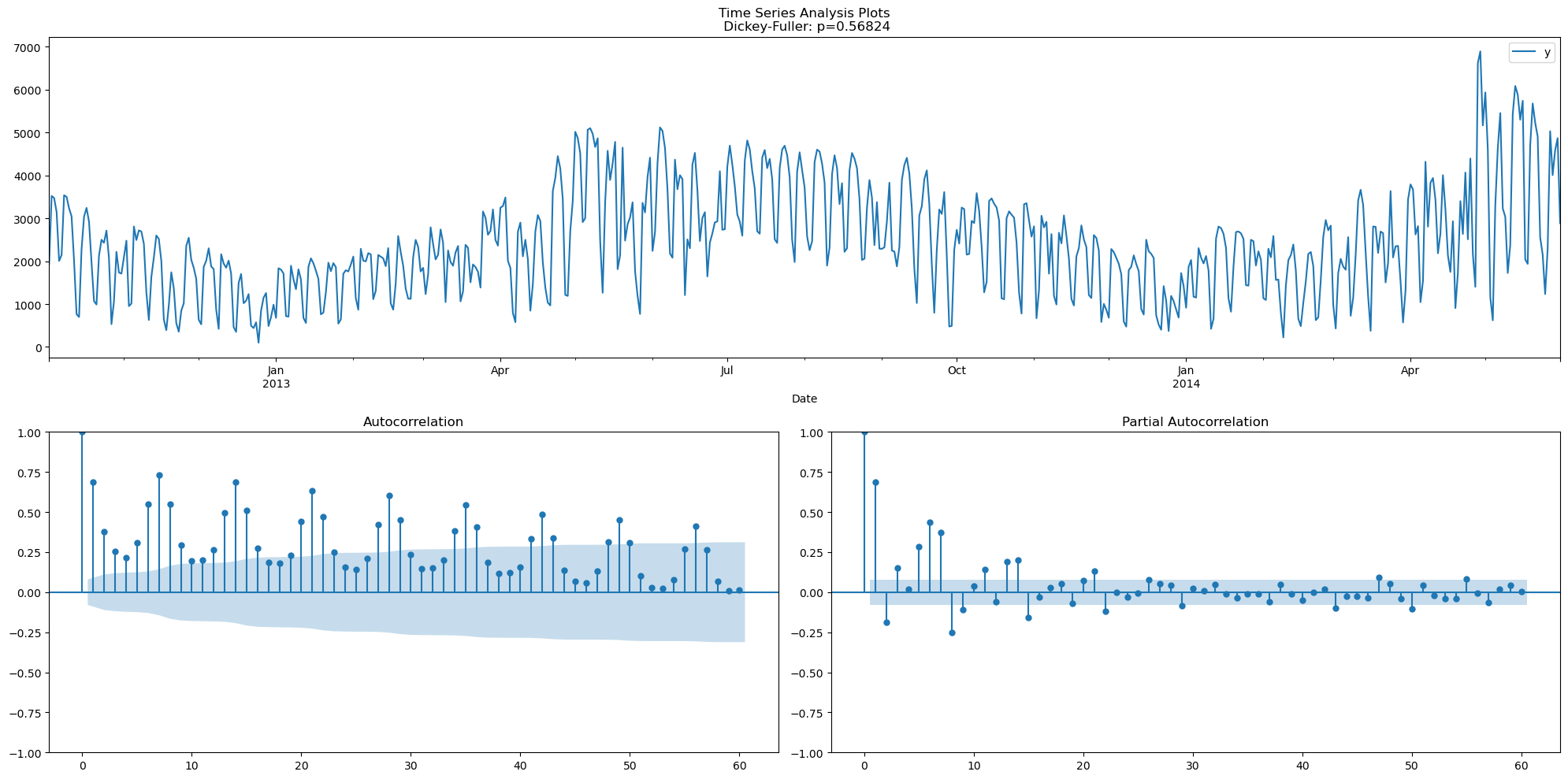

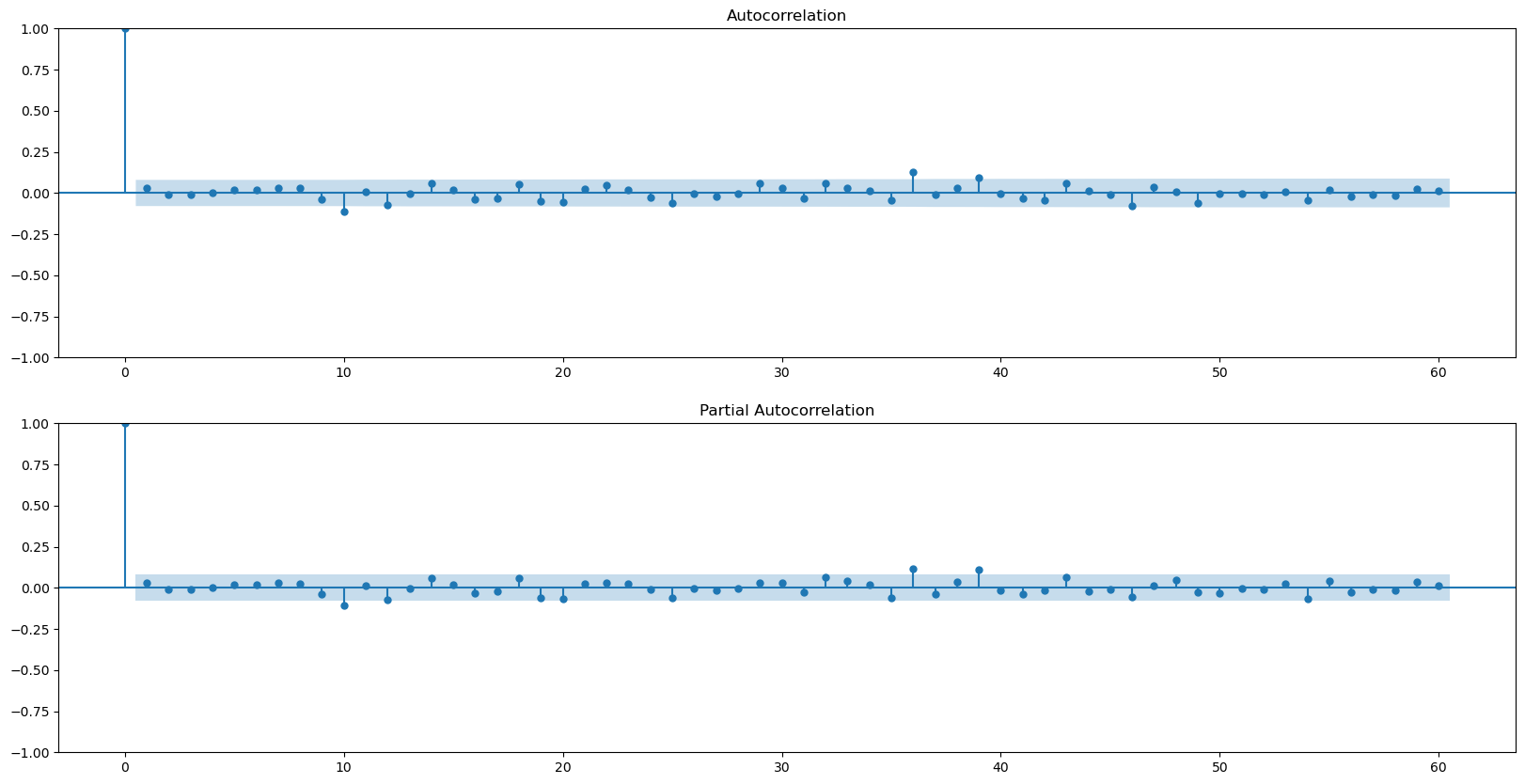

tsplot(df, lags=60)

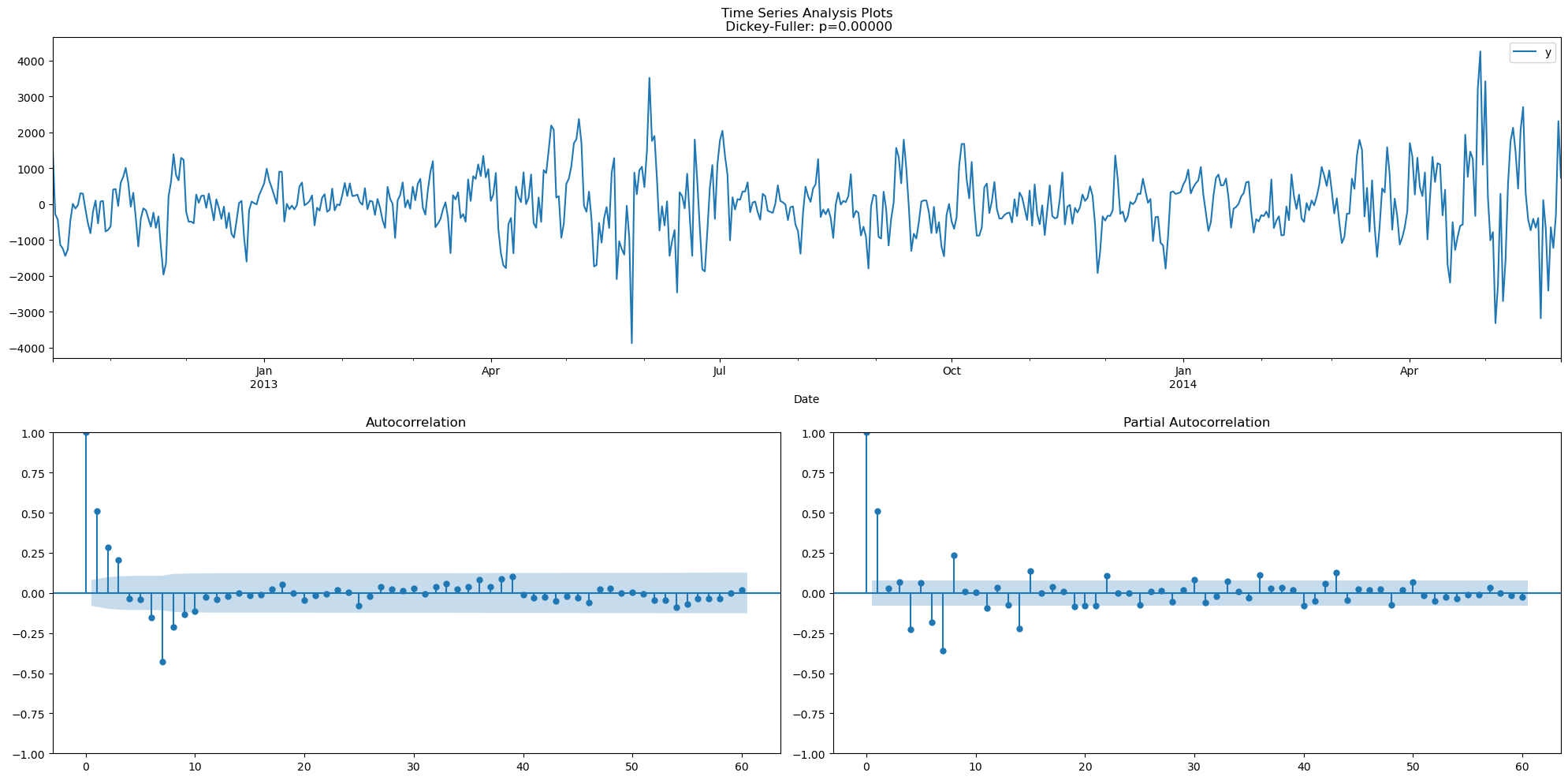

df_sdiff = (df - df.shift(7)).dropna()

tsplot(df_sdiff, lags=60)

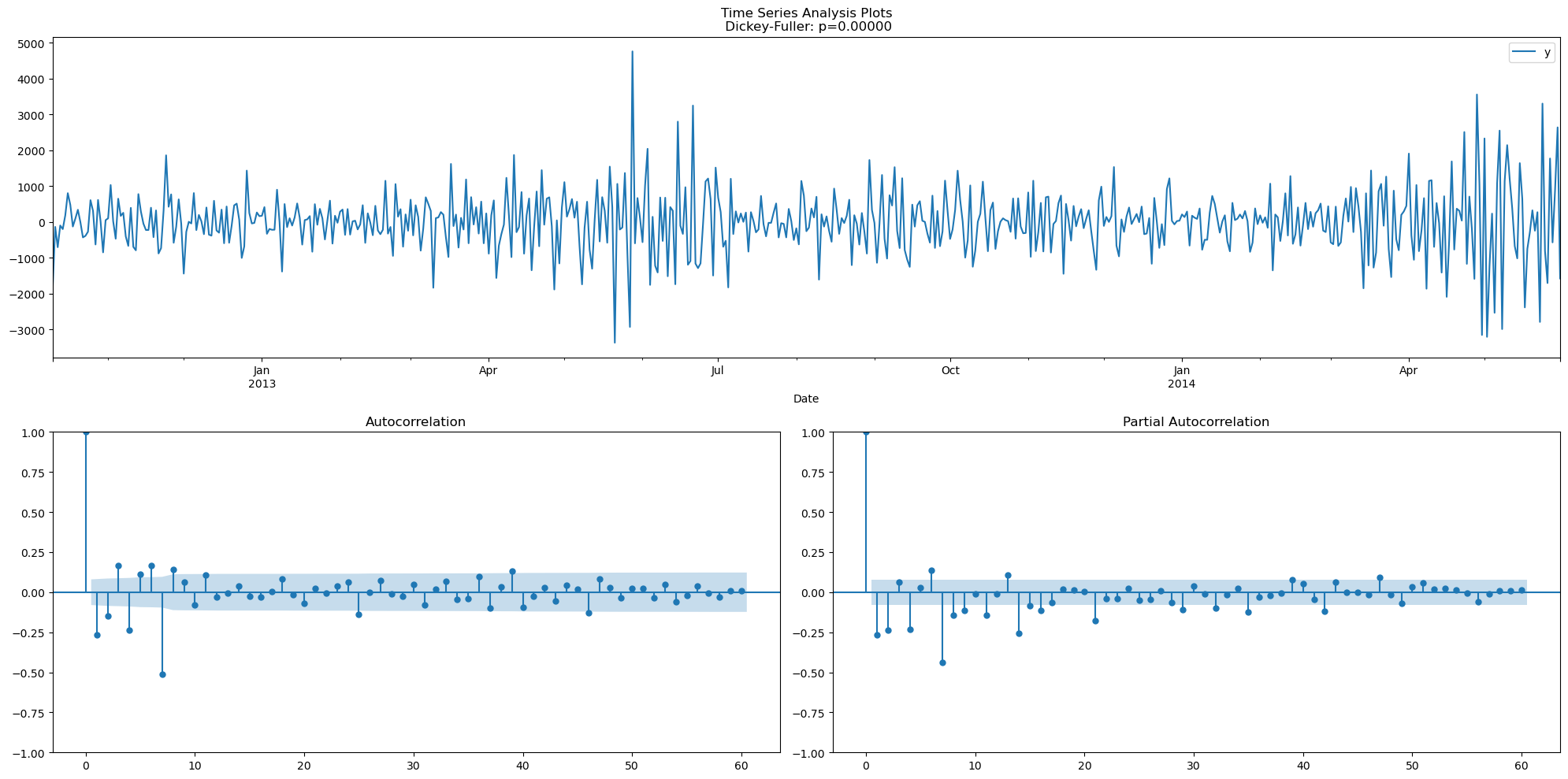

df_2diff = df_sdiff.diff().dropna()

tsplot(df_2diff, lags=60)

candidate_model = sm.tsa.statespace.SARIMAX(df, order=(0, 1, 6), seasonal_order=(0, 1, 1, 7)).fit()

candidate_model.summary()

C:\Users\silve\AppData\Roaming\jupyterlab-desktop\jlab_server\lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: No frequency information was provided, so inferred frequency D will be used.

self._init_dates(dates, freq)

C:\Users\silve\AppData\Roaming\jupyterlab-desktop\jlab_server\lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: No frequency information was provided, so inferred frequency D will be used.

self._init_dates(dates, freq)

| Dep. Variable: | y | No. Observations: | 607 |

|---|---|---|---|

| Model: | SARIMAX(0, 1, 6)x(0, 1, [1], 7) | Log Likelihood | -4671.220 |

| Date: | Sun, 03 Dec 2023 | AIC | 9358.439 |

| Time: | 23:58:25 | BIC | 9393.601 |

| Sample: | 10-02-2012 | HQIC | 9372.128 |

| - 05-31-2014 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ma.L1 | -0.3710 | 0.031 | -12.036 | 0.000 | -0.431 | -0.311 |

| ma.L2 | -0.2547 | 0.038 | -6.753 | 0.000 | -0.329 | -0.181 |

| ma.L3 | -0.0418 | 0.034 | -1.221 | 0.222 | -0.109 | 0.025 |

| ma.L4 | -0.2354 | 0.035 | -6.637 | 0.000 | -0.305 | -0.166 |

| ma.L5 | 0.0191 | 0.037 | 0.514 | 0.607 | -0.054 | 0.092 |

| ma.L6 | 0.0523 | 0.035 | 1.501 | 0.133 | -0.016 | 0.120 |

| ma.S.L7 | -0.9324 | 0.015 | -61.301 | 0.000 | -0.962 | -0.903 |

| sigma2 | 3.394e+05 | 1.35e+04 | 25.215 | 0.000 | 3.13e+05 | 3.66e+05 |

| Ljung-Box (L1) (Q): | 0.00 | Jarque-Bera (JB): | 219.02 |

|---|---|---|---|

| Prob(Q): | 0.99 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 2.29 | Skew: | -0.19 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 5.94 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

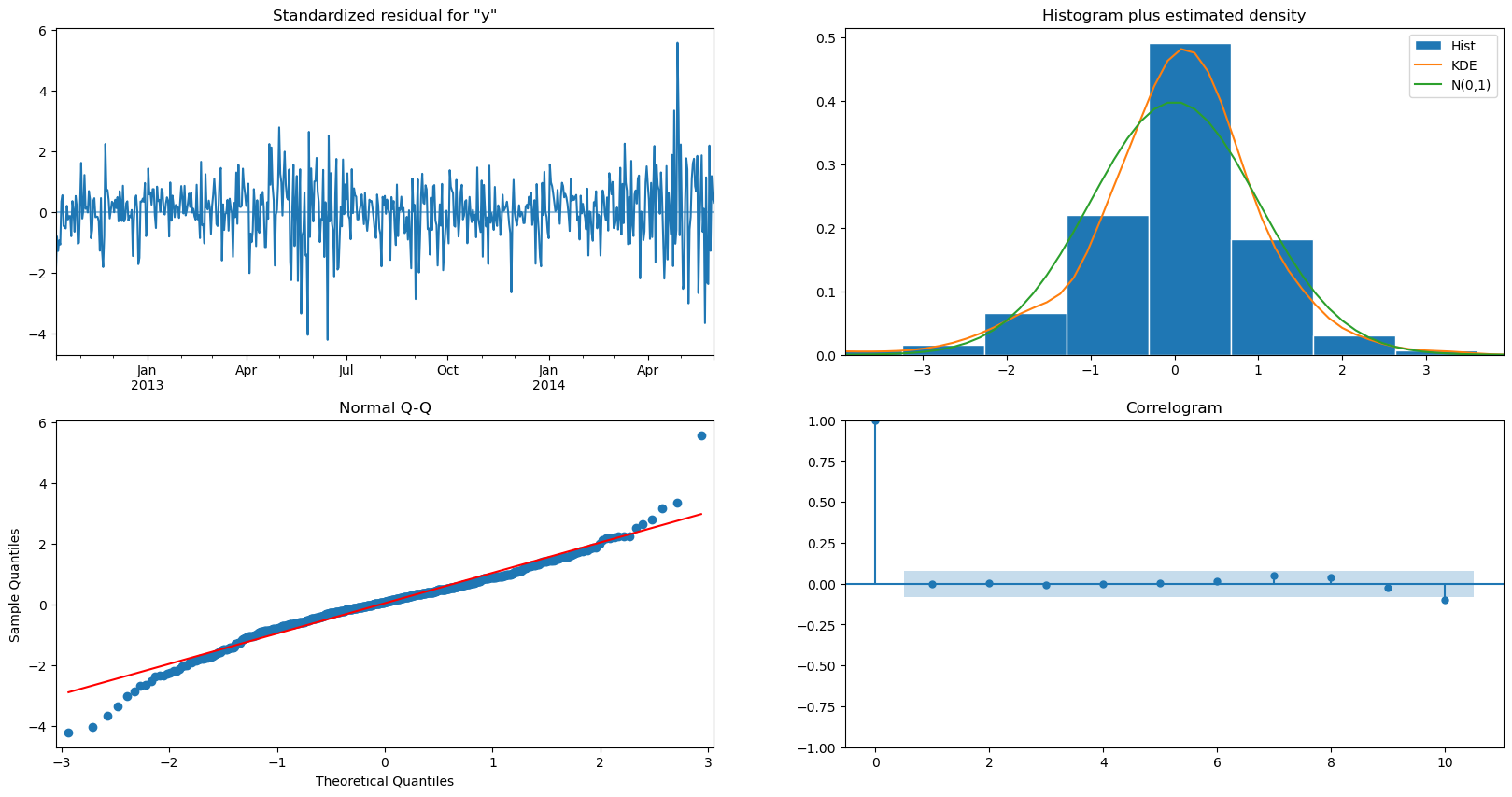

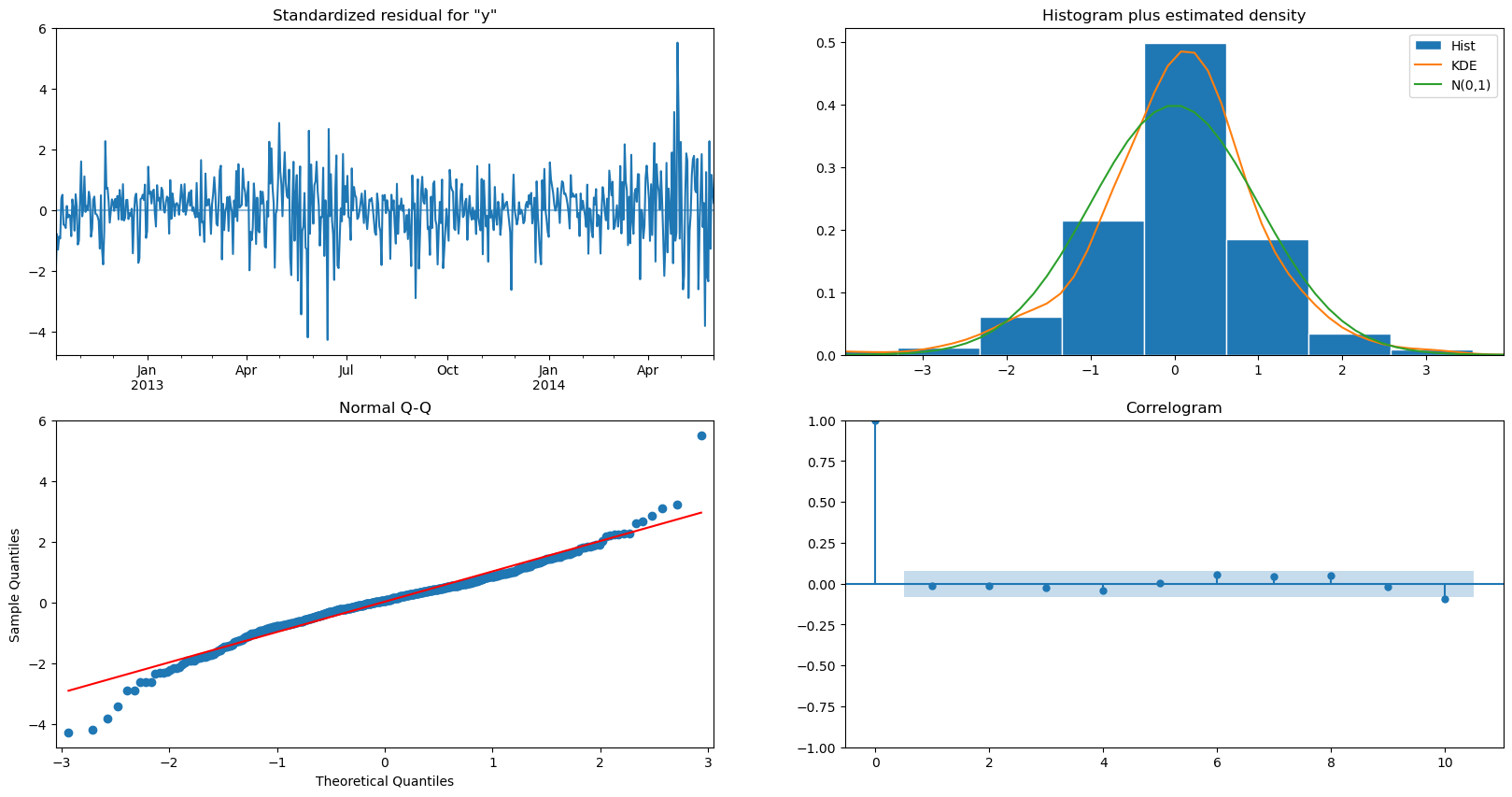

candidate_model.plot_diagnostics(figsize=(20,10))

plt.show()

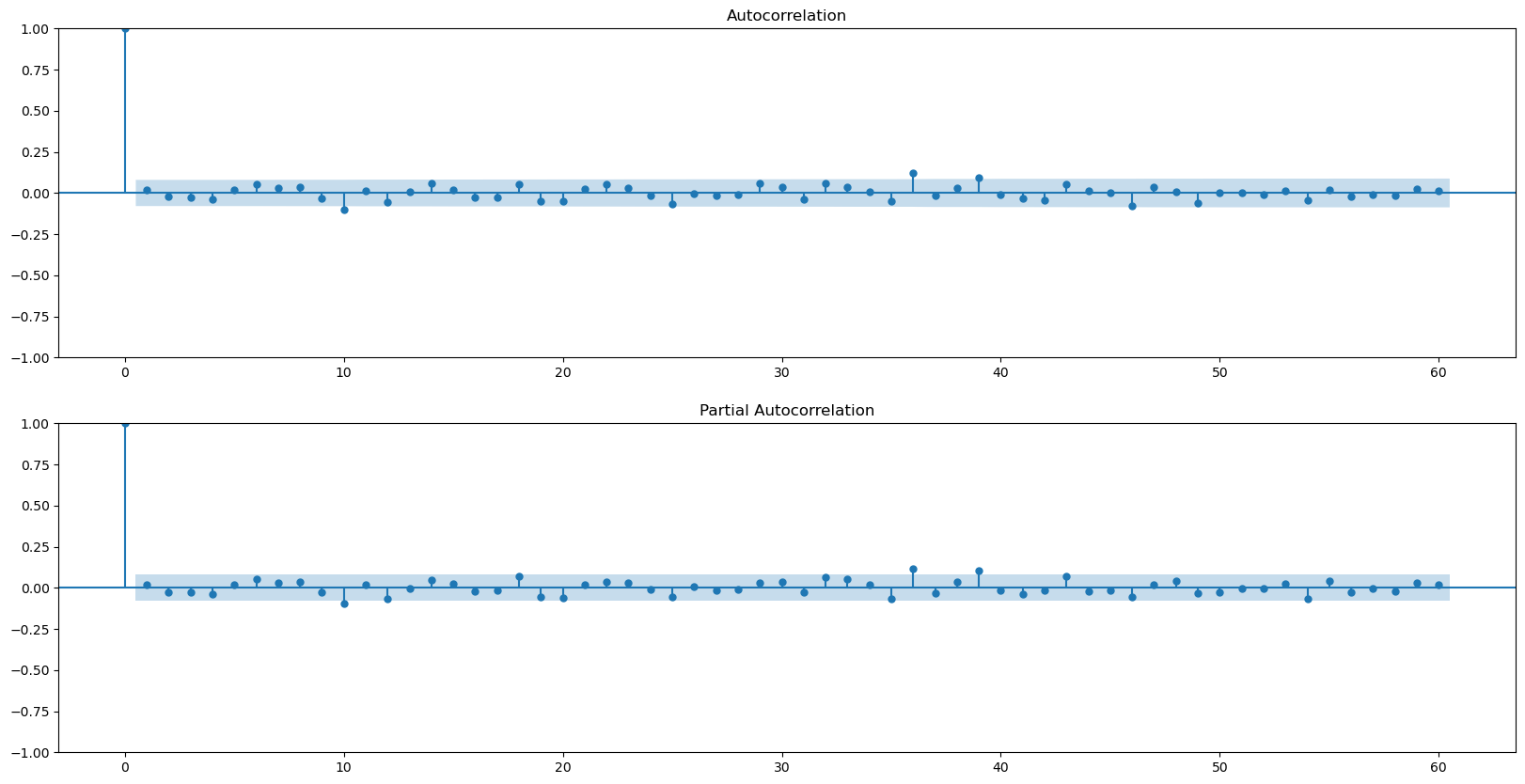

lags = 60

fig, axes = plt.subplots(2, 1, figsize=(20, 10))

smts.graphics.plot_acf(candidate_model.resid, lags=lags, ax=axes[0])

smts.graphics.plot_pacf(candidate_model.resid, lags=lags, ax=axes[1])

plt.show()

acorr_ljungbox(candidate_model.resid, lags=[2*7], return_df=True, model_df=6) # model_df = p + q

| lb_stat | lb_pvalue | |

|---|---|---|

| 14 | 15.647813 | 0.047708 |

candidate_model2 = sm.tsa.statespace.SARIMAX(df, order=(0, 1, 4), seasonal_order=(0, 1, 1, 7)).fit()

candidate_model2.summary()

C:\Users\silve\AppData\Roaming\jupyterlab-desktop\jlab_server\lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: No frequency information was provided, so inferred frequency D will be used.

self._init_dates(dates, freq)

C:\Users\silve\AppData\Roaming\jupyterlab-desktop\jlab_server\lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: No frequency information was provided, so inferred frequency D will be used.

self._init_dates(dates, freq)

| Dep. Variable: | y | No. Observations: | 607 |

|---|---|---|---|

| Model: | SARIMAX(0, 1, 4)x(0, 1, [1], 7) | Log Likelihood | -4672.557 |

| Date: | Sun, 03 Dec 2023 | AIC | 9357.114 |

| Time: | 23:58:28 | BIC | 9383.485 |

| Sample: | 10-02-2012 | HQIC | 9367.381 |

| - 05-31-2014 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ma.L1 | -0.3604 | 0.030 | -12.003 | 0.000 | -0.419 | -0.302 |

| ma.L2 | -0.2415 | 0.036 | -6.634 | 0.000 | -0.313 | -0.170 |

| ma.L3 | -0.0366 | 0.031 | -1.196 | 0.232 | -0.097 | 0.023 |

| ma.L4 | -0.2121 | 0.032 | -6.630 | 0.000 | -0.275 | -0.149 |

| ma.S.L7 | -0.9160 | 0.015 | -59.577 | 0.000 | -0.946 | -0.886 |

| sigma2 | 3.416e+05 | 1.34e+04 | 25.578 | 0.000 | 3.15e+05 | 3.68e+05 |

| Ljung-Box (L1) (Q): | 0.07 | Jarque-Bera (JB): | 229.44 |

|---|---|---|---|

| Prob(Q): | 0.79 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 2.30 | Skew: | -0.20 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 6.00 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

candidate_model2.plot_diagnostics(figsize=(20,10))

plt.show()

lags = 60

fig, axes = plt.subplots(2, 1, figsize=(20, 10))

smts.graphics.plot_acf(candidate_model2.resid, lags=lags, ax=axes[0])

smts.graphics.plot_pacf(candidate_model2.resid, lags=lags, ax=axes[1])

plt.show()

acorr_ljungbox(candidate_model.resid2, lags=[2*7], return_df=True, model_df=4) # model_df = p + q

---------------------------------------------------------------------------

AttributeError Traceback (most recent call last)

Cell In[13], line 1

----> 1 acorr_ljungbox(candidate_model.resid2, lags=[2*7], return_df=True, model_df=4) # model_df = p + q

File ~\AppData\Roaming\jupyterlab-desktop\jlab_server\lib\site-packages\statsmodels\base\wrapper.py:34, in ResultsWrapper.__getattribute__(self, attr)

31 except AttributeError:

32 pass

---> 34 obj = getattr(results, attr)

35 data = results.model.data

36 how = self._wrap_attrs.get(attr)

AttributeError: 'SARIMAXResults' object has no attribute 'resid2'

ps = range(0, 2)

qs = range(3, 6)

p = 0

d = 1

q = 4

Ps = range(0, 2)

Qs = range(0, 3)

P = 0

D = 1

Q = 1

s = 7

parameters = product(ps, qs, Ps, Qs)

parameters_list = list(parameters)

len(parameters_list)

def gs_arima(series, parameters_list, d, D, s, opt_method='powell'):

results = []

models = {}

best_aic = float("inf")

for param in parameters_list:

# we need try-except because on some combinations model might fail to converge

try:

model = sm.tsa.statespace.SARIMAX(

series,

order=(param[0], d, param[1]),

seasonal_order=(param[2], D, param[3], s)).fit(method=opt_method, disp=False)

except:

continue

aic = model.aic

if aic < best_aic:

best_model = model

best_aic = aic

best_param = param

results.append([param, model.aic])

result_table = pd.DataFrame(results)

result_table.columns = ['parameters', 'aic']

result_table = result_table.sort_values(by='aic', ascending=True).reset_index(drop=True)

return result_table, best_model

result_table, best_model = gs_arima(df, parameters_list, d, D, s)

result_table.head(10)

best_model.summary()

def mean_absolute_percentage_error(y_true, y_pred):

return np.mean(np.abs((y_true - y_pred) / y_true)) * 100

def plot_predictions(df, model, n_steps):

"""

Plots model vs predicted values

series - dataset with timeseries

model - fitted model

n_steps - number of steps to predict in the future

"""

data = df.copy()

data.columns = ['actual']

data['arima_model'] = model.fittedvalues

# forecast values

data['arima_model'][:s+d] = np.NaN

forecast = data['arima_model'].append(model.forecast(n_steps))

# calculate error, again having shifted on s+d steps from the beginning

error = mean_absolute_percentage_error(data['actual'][s+d:-n_steps], data['arima_model'][s+d:-n_steps])

plt.figure(figsize=(20, 10))

plt.title("Mean Absolute Percentage Error: {0:.2f}%".format(error))

plt.plot(forecast, color='r', label="model")

plt.axvspan(data.index[-1], forecast.index[-1], alpha=0.5, color='lightgrey')

plt.plot(data.actual, label="actual", alpha=0.8)

plt.legend()

plt.grid(True)

plot_predictions(pd.DataFrame(series), best_model, 60)